How to Make Your Kid a Millionaire by Age 35 (Yes, Really)

If you're a medical professional and either have kids or want kids someday, you've probably wondered:

How can I give them a financial head start I never had?

Let me show you how we’re doing it.

I’ve set up a system where both of my kids will be millionaires by the time they’re 35—and it doesn’t require hundreds of thousands of dollars.

It just takes intention, a few monthly contributions, and the right accounts.

First—This Is Not All or Nothing

Let me be clear:

You don’t need to hit millionaire status for this to be worth it.

Even if you can only do a fraction of this plan, you're still setting your kid up with a financial launchpad that most of us never had.

Even $100/month over time = six figures by adulthood. That’s still a huge win.

But if you do want to go all in, here’s exactly how we’re making millionaire status happen by age 35:

Step 1: Open a UTMA Account

We start with a UTMA account (Uniform Transfers to Minors Account)—

✅ It’s flexible

✅ It’s taxable

✅ And the mone...

How to Build Wealth When the Economy Feels Like a Dumpster Fire

Spring 2025 came in hot with tariff wars, rising inflation, student loan chaos, and stock market volatility that has a lot of medical professionals wondering...

“Is it even possible to build wealth in a season like this?”

Short answer: yes.

But you need a strategy—and some serious emotional discipline.

Why Personal Economics > Macroeconomics

The truth? You could come out of this economic mess ahead—if you have your personal financial systems dialed in.

✅ No high-interest debt

✅ 3–6 months of cash reserves

✅ Multiple income streams

✅ A student loan plan

✅ A long-term investing system

If you don’t have these in place, this season can wreck you.

If you do? You can use it to build wealth while everyone else panics.

What Investing in a “Down Market” Actually Feels Like

Whether you’re:

- A new investor putting in your first $1,000

- Or a seasoned one watching $70K disappear from your account in a day

It still stings.

But this is where people either panic and pull out...

Or keep go...

What Most New Grad PAs Realize After Their First Paycheck

You graduate. You pass your boards. You land the job.

That six-figure paycheck hits—and then... reality sets in.

If you’re a brand new PA, you know exactly what I’m talking about.

It’s not quite the dream you imagined. Expenses feel overwhelming. Loans are looming. And you’re wondering, “Wait… where did my paycheck go?”

Let’s walk through exactly what you should be doing in your first year of practice to get your money right.

Why Generic Budget Rules Don’t Work for PAs

You’ve probably heard of those 50/30/20 budgeting rules:

- 50% to needs

- 30% to wants

- 20% to savings/investing

I hate those.

They’re made for the masses—not for people like us.

If I followed that rule? I wouldn’t be a millionaire by 31. I needed a lot more than 20% going toward debt and wealth-building.

What you really need is a cash flow system that helps you grow your net worth—not just track your spending.

Inside the Millionaires in Medicine Club, I break down exactly how to do this with a free tracker you c...

How I’m Making My Kids Millionaires... Without Spoiling Them

Yep, you read that right. It's totally possible to turn your kid into a future millionaire—without needing to throw in hundreds of thousands.

I’m doing it with just a few thousand dollars and a lot of intention. And in this blog, I’ll show you exactly how:

👉 The accounts we use

👉 The money system we teach our 3-year-old

👉 And the mindset shifts that actually matter more than the money

Let’s break it all down.

Our Four-Bucket Money System for Kids

You’ve probably heard of the classic give-save-spend system for teaching kids about money.

I hate it.

Why? Because it completely ignores investing—arguably the most important pillar of long-term wealth.

So instead, we created our own version: Give, Save, Spend, and Invest.

Every Sunday, our 3-year-old gets her allowance in quarters (supervised, of course), and she gets to divide those coins between her four jars.

To make the “invest” jar feel real, we created a visual thermometer tracker for her investing goals, broken into:

- 🎓 Coll...

How PAs, NPs, and Pharmacists Are Building Millions (Even Without High Salaries)

If you’re a PA, NP, or pharmacist and think wealth building is only for people in higher-paying specialties or dual-income households with no debt—this blog is for you.

The truth? It’s 100% possible to become a multi-millionaire with a six-figure income, even if you’re working in primary care, living in a high cost-of-living area, or just starting out. How do we know? Because we’ve helped medical professionals just like you do exactly that.

Below are five real client case studies to show you what’s possible with the right systems, strategy, and support.

CASE 1: Kelly, a Primary Care PA, Married to an RN

Challenge: Lower-paying specialty + early 30s with limited investments

Goals: Reduce hours when they start a family, retire early with flexibility

What We Did:

- Optimized their PSLF strategy to save $600/month on student loan payments

- Reallocated that money into an investing system

- Completely overhauled their account structure and monthly contributions

Result:

Kelly and her sp...

Why I Stopped Paying for Someone To Manage My Investments, and Saved Over $1.5 Million

If you're a PA, NP, or pharmacist and you've ever thought, "Personal finance is just too complicated for me," you're not alone. That’s exactly what most of us are conditioned to believe.

But here's the truth: learning to manage your own money could save you more than $1.5 million in your lifetime. I know this because I’ve lived it.

My Story: From Student Debt to Seven Figures

When I graduated as a critical care PA, I had $161,000 in student loans and zero assets. Like many new grads, I was eager to "do the right thing", so I hired a financial advisor and opened a Roth IRA through Edward Jones.

It felt like I was checking all the right boxes. But years later, I realized I had paid thousands in fees without even realizing it: fees that were quietly dragging down my returns.

Once I learned to manage my portfolio myself, everything changed. Less than a decade later, I hit $1 million in net worth at age 31.

The Cost of Not Learning Personal Finance

Most medical professionals fall int...

Can You Really Become a Multi-Millionaire as a PA, NP, or Pharmacist?

When I first became a PA, I thought hitting $1 million in net worth would mean I “made it.”

But now that I’ve actually crossed that milestone, and helped hundreds of medical professionals do the same. I can tell you this:

A million dollars isn’t enough.

If you want to retire comfortably (or early), reduce your clinical hours, or stop working when your health is still good, you’ll probably need $3–4 million or more.

Let’s break down why that number matters, and how I built wealth faster than most people thought possible.

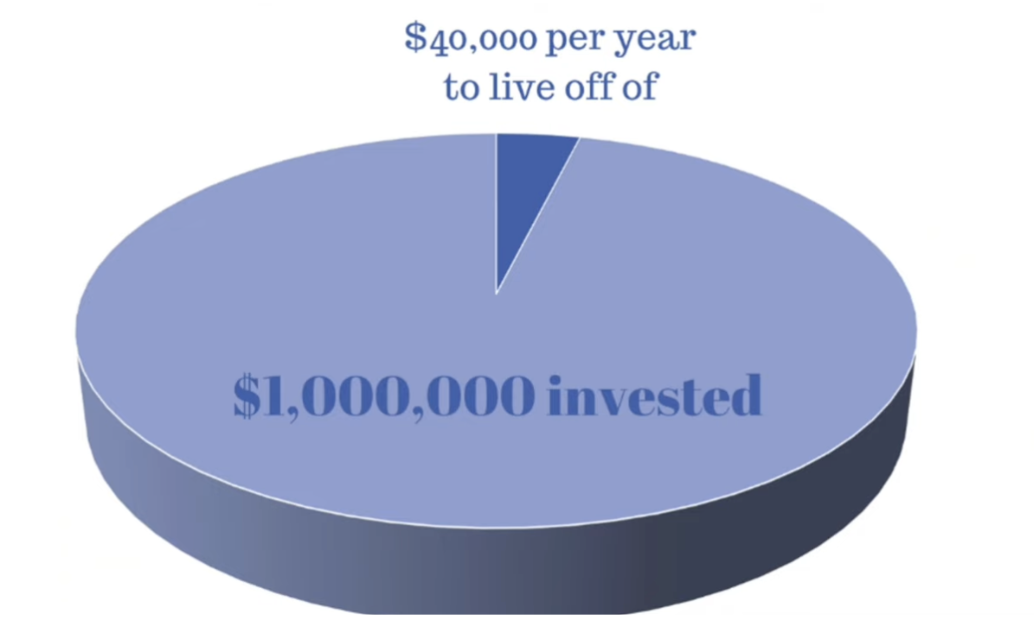

Why $1M Won’t Cut It Anymore

Here’s what most people don’t realize:

If you retire with $1 million, and use the standard 4% withdrawal rule, that gives you just $40,000/year to live on. Not exactly luxurious.

Now add inflation into the mix.

What feels like enough today won’t go nearly as far by the time we’re 65.

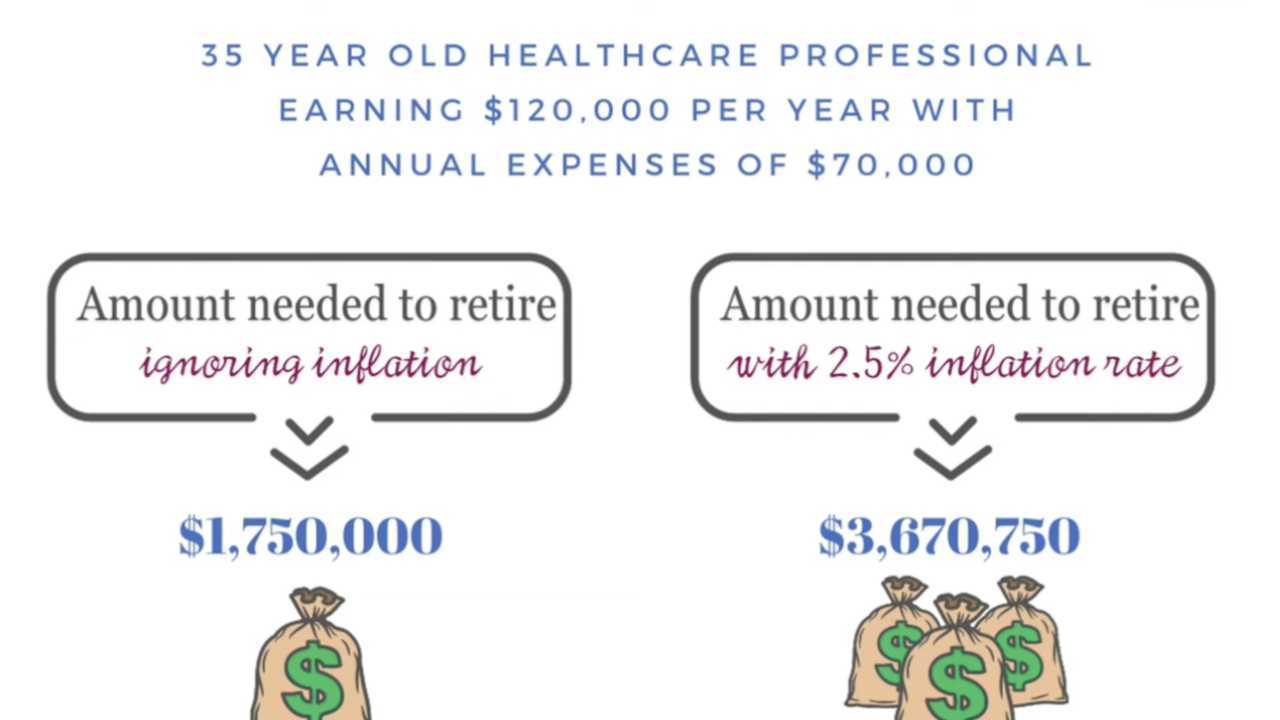

Example:

At 35 years old, if I spend about $70K/year, I’d need $3.7M by age 65 to maintain that lifestyle.

At 35 years old, if I spend about $70K/year, I’d need $3.7M by age 65 to maintain that lifestyle.

(That’s the inflation-adjusted cost.)

So no…...

How Medical Professionals Can Earn $10K+ a Year in Passive Income (Without Working More)

How Medical Professionals Can Earn $10K+ a Year in Passive Income (Without Working More)

What if your money could work harder, so you don’t have to?

Whether your goal is an extra $10K, $20K, or $50K/year, building passive income as a PA, NP, pharmacist, or physician is 100% possible. But not all passive income streams are created equal.

In this post, we’re breaking down the top 3 cash-flowing investment strategies that medical professionals are using in 2025 to earn more: without picking up extra shifts.

1. Dividends from the Stock Market – True Passive Income

Barrier to entry: Low

Truly passive: ✅

Tax advantages: ✅ (qualified dividends = long-term capital gains rate)

But here’s the catch:

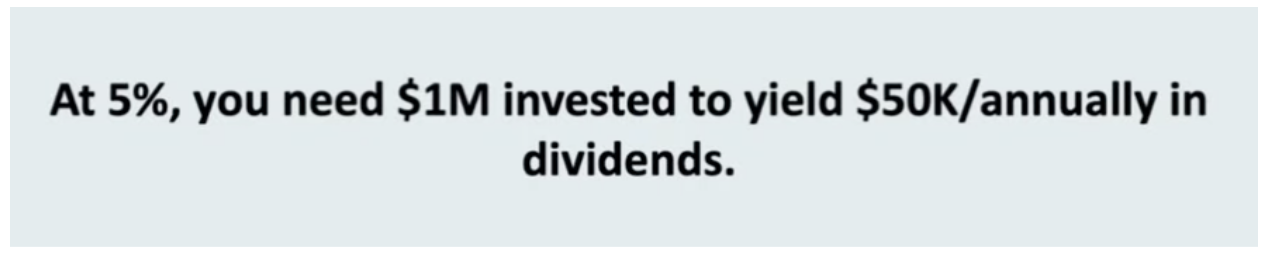

To earn $50K/year from dividends, you’d need to invest $1 million at a 5% dividend yield. Most people can’t do that in the early wealth-building years.

This is the easiest place to start. Open a brokerage through Fidelity, Vanguard, or Schwab and invest in ETFs and index funds that pay divi...

How to Plan a Money Date: Build Wealth and a Stronger Relationship

As a PA-C and money expert,, I’ve worked with thousands of medical professionals who are trying to juggle busy lives, growing careers, and massive student loans. But there’s one thing my husband and I started doing years ago that changed everything in our relationship and our finances:

We started having quarterly money dates.

It’s not just about budgets. It’s about alignment, goal setting, and long-term wealth building…. together.

What Is a Money Date (And Why Every Couple Needs One)?

A money date is a structured yet relaxed time to check in with your partner about money without distractions or stress. It’s a chance to:

- Celebrate financial wins

- Review spending & progress

- Set clear, intentional goals

- Avoid miscommunication about money

- Stay on the same page (and build real wealth)

And when done right? It turns “you and me” into a financially unstoppable we.

How Often Should You Do It?

Quarterly is ideal. Once every 90 days keeps things on track without being overwhelmin...

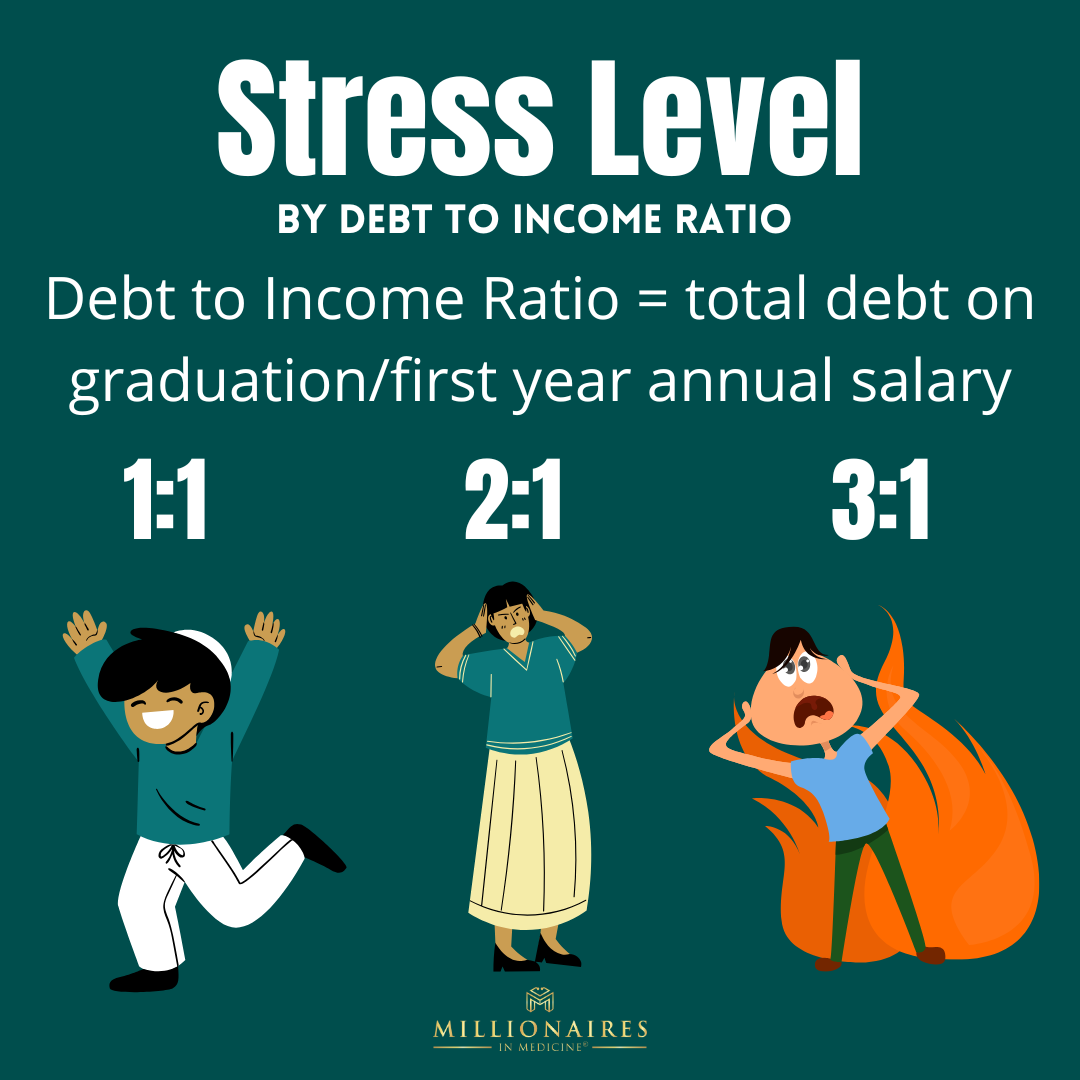

The One Student Loan Metric Every New Grad PA-C & Medical Professional Needs to Know

If you’re a new grad PA, NP, PharmD, or medical professional trying to figure out how the heck you’re supposed to manage your student loans… there’s one number that changes everything:

Your Debt-to-Income Ratio.

This simple calculation determines:

✅ Whether PSLF is worth it

✅ If private practice is even an option

✅ How painful your monthly payments will be

✅ And how much flexibility you’ll actually have in your career

Let’s break down why debt-to-income ratio (DTI) matters so much, especially if you're just starting out.

What Is Debt-to-Income Ratio (DTI) for Medical Professionals?

Your debt-to-income ratio is your total student loan debt divided by your anticipated annual income.

Example:

If you graduate with $100K in student loans and expect to earn $100K as a PA, your DTI is 1:1.

If you have $200K in loans, and still earn $100K, your DTI is 2:1.

🎯 Key tip: Use starting salary, not median salary, especially if you’re still in school or early in your career.

The Ideal DTI Rat...

Author

Kristin Burton

Founder

Kristin Burton is a pulmonary/critical care PA and founder of Millionaires in Medicine. She paid off $161,000 in student loan debt in 16 months, and then went on to become a millionaire at 31.

Have insurance needs?

Look no further than Protuity for your life and disability insurance.

Navigating physician contracts can be overwhelming. Resolve offers a personalized legal experience to equip you with the tools and support needed to secure the best terms for your career.

Use code MIM15 to receive a 15% discount at checkout.

Doc2Doc helps healthcare providers explore personal loan options to consolidate debt, simplify payments, and potentially lower what they’re paying in interest.

Prepping for EORs, PANCE, PANRE, or EOC?

Get the support you need right now to stop second guessing your test answers, ditch your anxiety, and learn the 7 critical test-taking skills you need to knock your PA exams out of the park.