PA Specialties Salary 2026: The Highest and Lowest Paying Careers — And What Actually Builds Wealth

PA Specialties Salary 2026: The Highest and Lowest Paying Careers — And What Actually Builds Wealth

I became a millionaire at 31 on a PA salary.

Not a physician salary. A PA salary (in cardiology and critical care) built by choosing the right specialty, understanding my contract, and getting strategic with investing.

Most PA salary articles are going to stop at the number. They'll show you a ranking, hand you a table, and call it a day. But the number on your offer letter is not the same as the money you actually keep. And the money you keep is not the same as the wealth you build.

This is the full picture: the highest and lowest paid PA specialties in 2026, the states where your dollar goes furthest, the contract structures that separate the top earners from everyone else, and the compensation levers most PAs never think to negotiate… or even ask about.

Quick Answer: Highest-Paid PA Specialties in 2026

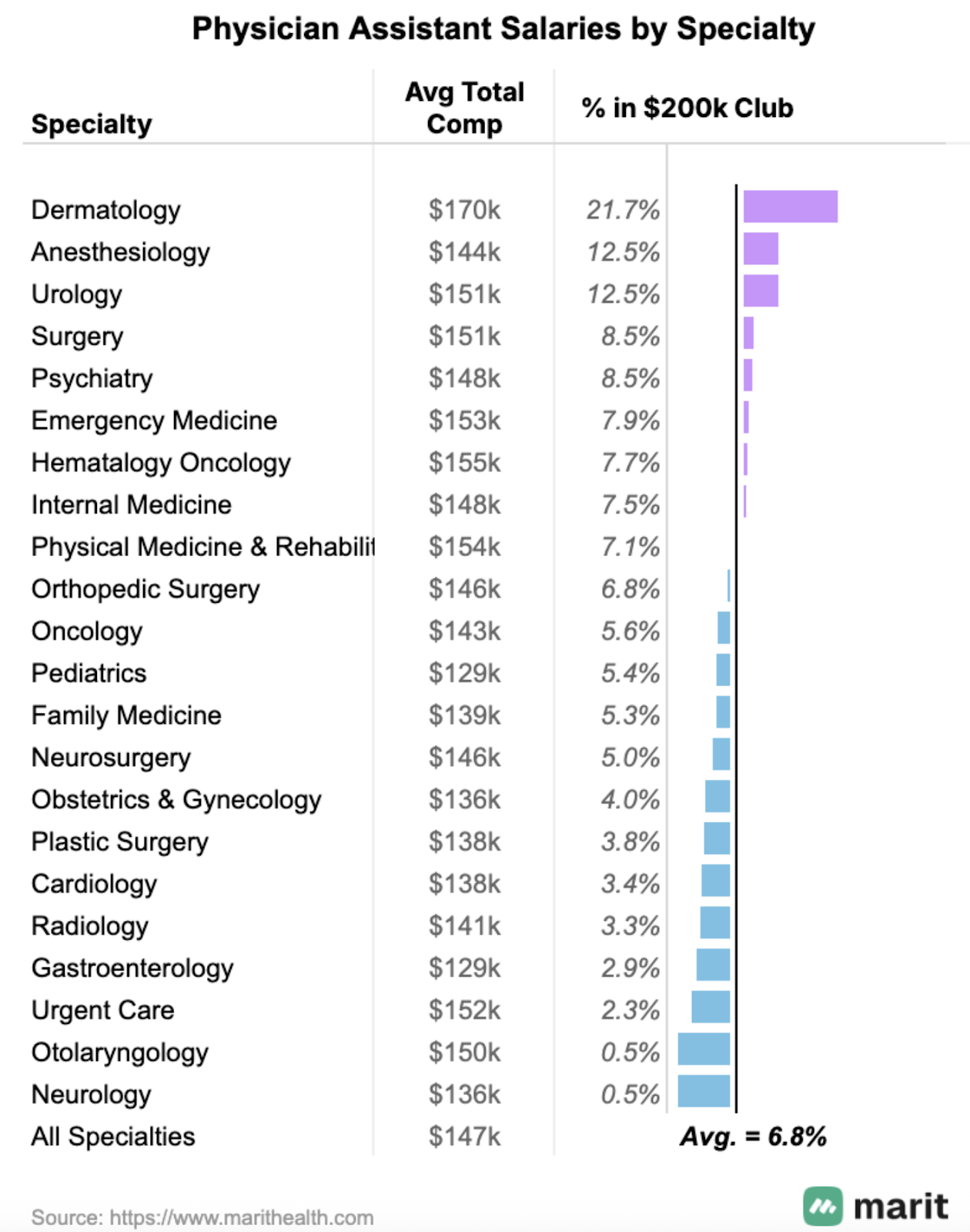

Based on data from Marit Health, the top five earning PA specialties in 2026 ...

How PAs Can Make Money in Legal Medicine Without Leaving Clinical Practice

If you’re a PA looking for a high-paying side hustle that doesn’t require extra shifts, legal medicine is one of the most interesting options out there.

Why?

Because it lets you use the clinical expertise you’ve already built — but in a nonclinical way that can often be done from home and pays far more per hour than most clinical work.

In this conversation, I sat down with Susan Ferrero, a PA with 20 years of experience who built her own path into the medical-legal space and now runs Ferrero Medical Consulting full-time.

If you’ve ever wondered whether there’s a way to turn your clinical experience into flexible nonclinical income, this is a path worth knowing about.

What Is Legal Medicine for PAs?

At the simplest level, legal medicine means helping attorneys understand medical cases.

That can include:

- reviewing records

- analyzing whether care met the standard

- writing reports

- serving as an expert witness

- helping explain medical concepts in legal cases

And despite what m...

Don’t Sign That Contract Yet: The Scope + Pay “Ramp” That Saves Medical Pros From Getting Burned

If you’ve ever taken a job that looked perfect on paper… but felt awful in real life?

This is for you.

As a PA with nearly a decade in hospital medicine, critical care, and cardiology — I’ve signed a lot of contracts. I’ve also worked multiple PRN/per diem jobs, and through Millionaires in Medicine, I’ve helped hundreds of medical professionals navigate their careers.

So yes… I’ve seen the good, the bad, and the ugly.

Before you sign your next contract, you need to understand one concept that prevents most job regret:

Your scope of practice ramp + your compensation ramp.

If those two don’t grow together, you’ll eventually feel trapped — clinically, financially, or both.

The #1 Contract Mistake Medical Professionals Make

Most clinicians focus on the salary number and stop there.

But the real question is:

“What does this job become in 1–2–3–4 years?”

Your scope should expand as your skills expand. Your pay should expand as your value expands.

If your employer has no plan for ...

The Epidemic of Politeness Costing PAs Tens of Thousands in Pay

Most physician assistants don’t earn less because they aren’t valuable.

They earn less because they’re too polite to ask.

I’ve seen it over and over again—smart, capable PAs leaving tens of thousands of dollars on the table simply because negotiation feels uncomfortable, intimidating, or “ungrateful.”

I’m Kristin Burton, PA-C, and I’ve been a PA for nearly a decade. I’ve negotiated primary jobs, per diem roles, investment deals, and business contracts. And I can tell you this with certainty:

Failing to negotiate doesn’t just affect your next paycheck—it compounds into decades of under-earning and lost wealth.

Why Negotiation Feels So Hard for PAs

I still remember my first PA job offer.

I was on rotation when the email hit my inbox. My heart was racing. I was thrilled. They could have offered me almost any number and I would’ve said yes.

I was just grateful to have a six-figure job as a new grad.

Negotiation wasn’t even on my radar.

And that mindset—“Where do I sign?”—follows ...

Should Medical Professionals Consider a 50-Year Mortgage? The Truth No One’s Telling You

What if you could finally afford your actual dream home — not the starter home, not the condo, but the home with the extra space, the yard, and the room to breathe?

And what if the monthly payment felt like rent?

That’s the promise behind the new 50-year mortgage being proposed. On the surface, it sounds like a solution for medical professionals struggling with high home prices, rising interest rates, and student loan debt.

But is it actually a good idea?

Let’s walk through the real numbers.

Why Housing Feels Impossible for Medical Professionals

Home prices have jumped 30–50% since 2020.

Interest rates climbed.

Saving a six-figure down payment as a new grad PA, NP, CRNA, or PharmD feels unrealistic.

So the 50-year mortgage claims to “solve” affordability by lowering monthly payments.

But lowering payments always comes with a cost.

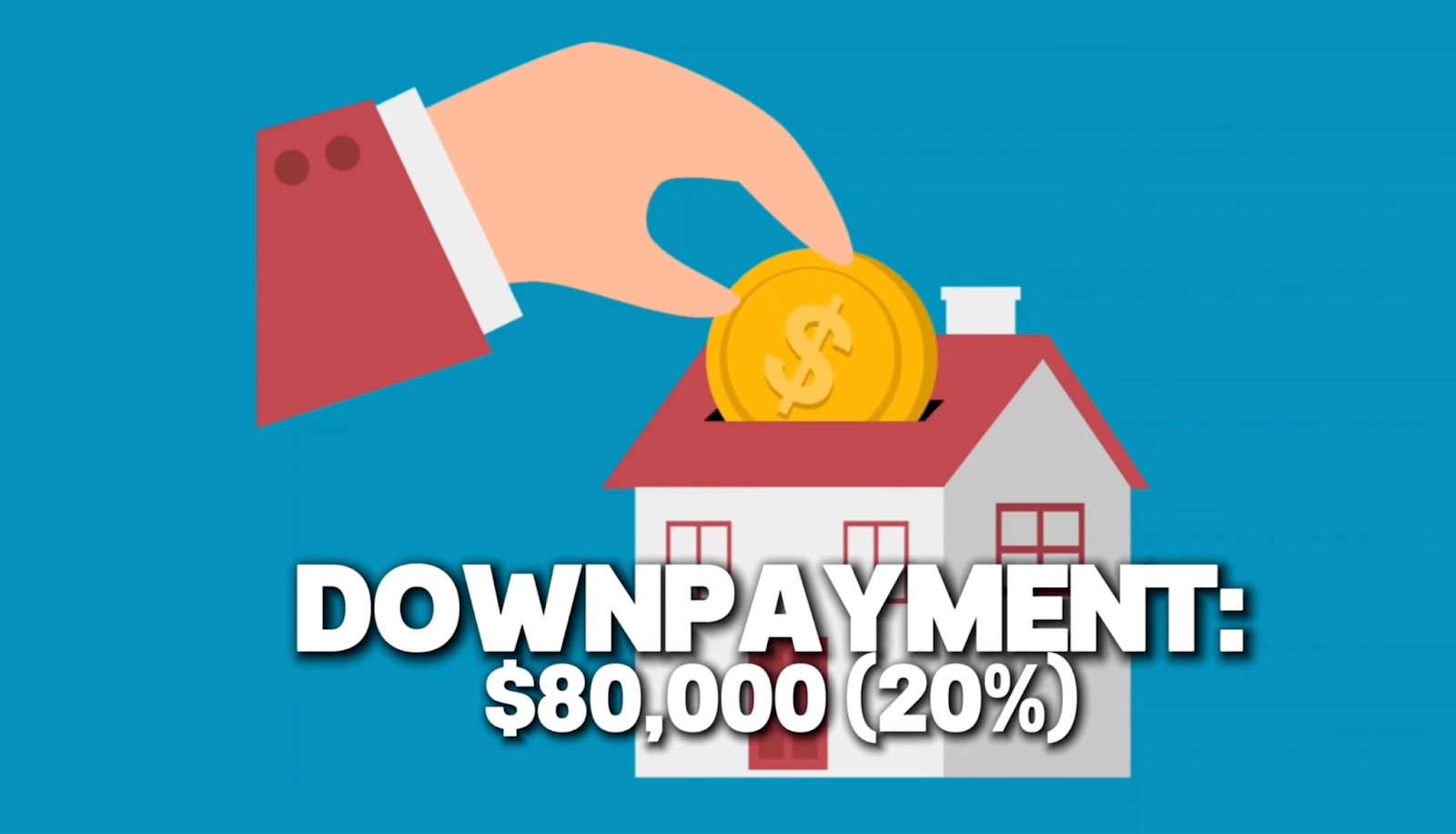

What a 50-Year Mortgage Really Means for a $400K Home

Assume:

- Home price: $400,000

- Loan: $320,000 (20% down)

- Interest rate: 6.5%

30-Year Mo...

Are You Underpaid? The 6-Step Salary Check Every PA, NP, and PharmD Needs

📉 You might be underpaid by $10,000—or more.

If you're a PA, NP, or pharmacist and you're relying on vibes and guesswork instead of real data to evaluate your compensation, you could be losing tens of thousands of dollars every year. That’s money that could be funding your investments, knocking out debt, or helping you reach financial independence faster.

So let’s fix that.

Below is the 6-step system to figure out what you should be earning—and what to do if you're falling short.

Step 1: Find the Median Salary for Your Subspecialty

First, you need a benchmark.

It’s shocking how many medical professionals skip this part. Before asking friends or Facebook groups if a salary is “good,” go to actual data sources.

📊 Try:

- MaritHealth’s Salary Explorer (most granular + updated for 2025)

- AAPA Salary Report

- Bureau of Labor Statistics

- Salary.com

- Glassdoor’s Know Your Worth tool

For example:

- 🩺 CT Surgery PA Median = $158,000

- 👶 Pediatric PA Median = $127,000

👉 Write this num...

The Debt Avalanche Strategy Every Medical Professional Needs to Know in 2025

If you're a PA, NP, or pharmacist with any debt that's causing you stress, this guide is for you.

Forget random payment orders or blind budgeting apps. It's time to get strategic about your debt and your future wealth. In this blog, you'll learn the smarter way to tackle debt (hint: it's not the snowball method), how to save thousands in interest, and when to start investing while still paying off loans.

Snowball vs. Avalanche: What Actually Saves You Money?

You've likely heard of the Debt Snowball, a method where you pay off the smallest debt first regardless of interest rate. It's emotionally satisfying, sure. But if you're carrying any high-interest debt (like credit cards or personal loans), it's costing you thousands more over time.

Instead, opt for the Debt Avalanche strategy:

- Step 1: List your debts from highest to lowest interest rate (not balance).

- Step 2: Make minimum payments on all debts.

- Step 3: Throw all extra payments at the highest-interest debt first.

💡 Exa...

How to Save as a PA-C (or Any Medical Professional Earning $100K+)

If you're a PA, NP, or pharmacist earning over $100K a year but your savings account still looks like it belongs to your student days... you're not alone.

I became a millionaire by age 31, not by winning the lottery or flipping houses—but by mastering the basics: saving, investing, and being intentional with money. In this post, I’ll walk you through how to calculate your real savings rate, strategies to save more without sacrificing joy, and how to build wealth faster.

Step 1: Know Your Actual Savings Rate

Most medical professionals have no idea what their savings rate is. If that’s you? Let’s fix that.

To find your savings rate:

- Add up ALL dollars you put toward true savings and investments each month. That includes:

- Emergency fund deposits (your sinking funds for vacations don’t count)

- 401(k), 403(b), or other employer retirement plan contributions

- Roth IRA or brokerage account deposits

- HSA contributions

- Then divide that number by your gross monthly income (not your ...

From $0 to $1.2M in 7 Years: How PAs Can Become Millionaires Faster Than You Think

What if I told you that it’s possible to go from zero to over a million dollars invested in just 7 years on a PA salary?

No gimmicks. No crazy frugality. No lottery luck.

Just a clear, proven 3-step strategy any driven PA can follow.

Let’s break it all down.

Step 1: Cross the $200K Mark with Your Primary Job

This is where most PAs tap out, but it’s also where the biggest growth potential starts.

📊 According to data from Marit Health, 1 in 14 PAs already earn over $200K/year.

Here’s how to increase your odds of joining them:

✅ Choose a High-Earning Specialty:

Dermatology, critical care, cardiothoracic surgery, and PM&R consistently top the list. But it’s not just about the specialty—it’s about where you land within it.

💡 Specialties like dermatology, plastic surgery, and psychiatry have high intraspeciality variance in pay, meaning some PAs are crushing $200K+ while others are barely above average. Don’t just switch specialties… switch to a better-paying role within your speci...

Top Paying PA Specialties in 2025: Where Physician Associates Are Earning the Most (and Least)

If you're a practicing PA, a PA student, or even considering PA school, you're probably asking yourself: Is the debt worth it? The good news? PA salaries are going up. The better news? You have more control over your income than you might think.

PA Salaries Are On the Rise (But Uneven)

According to the latest AAPA Salary Report, PA earnings rose 5.5% in 2024 alone. MGMA data shows:

- Surgical PAs: median is up 15% since 2020

- Non-surgical, non-primary care PAs: median is up 21%

- Primary care PAs: median is up 30%

Sounds great for primary care, right? Not so fast. That percentage growth only tells part of the story. You need to look at absolute numbers and actual earning potential across subspecialties.

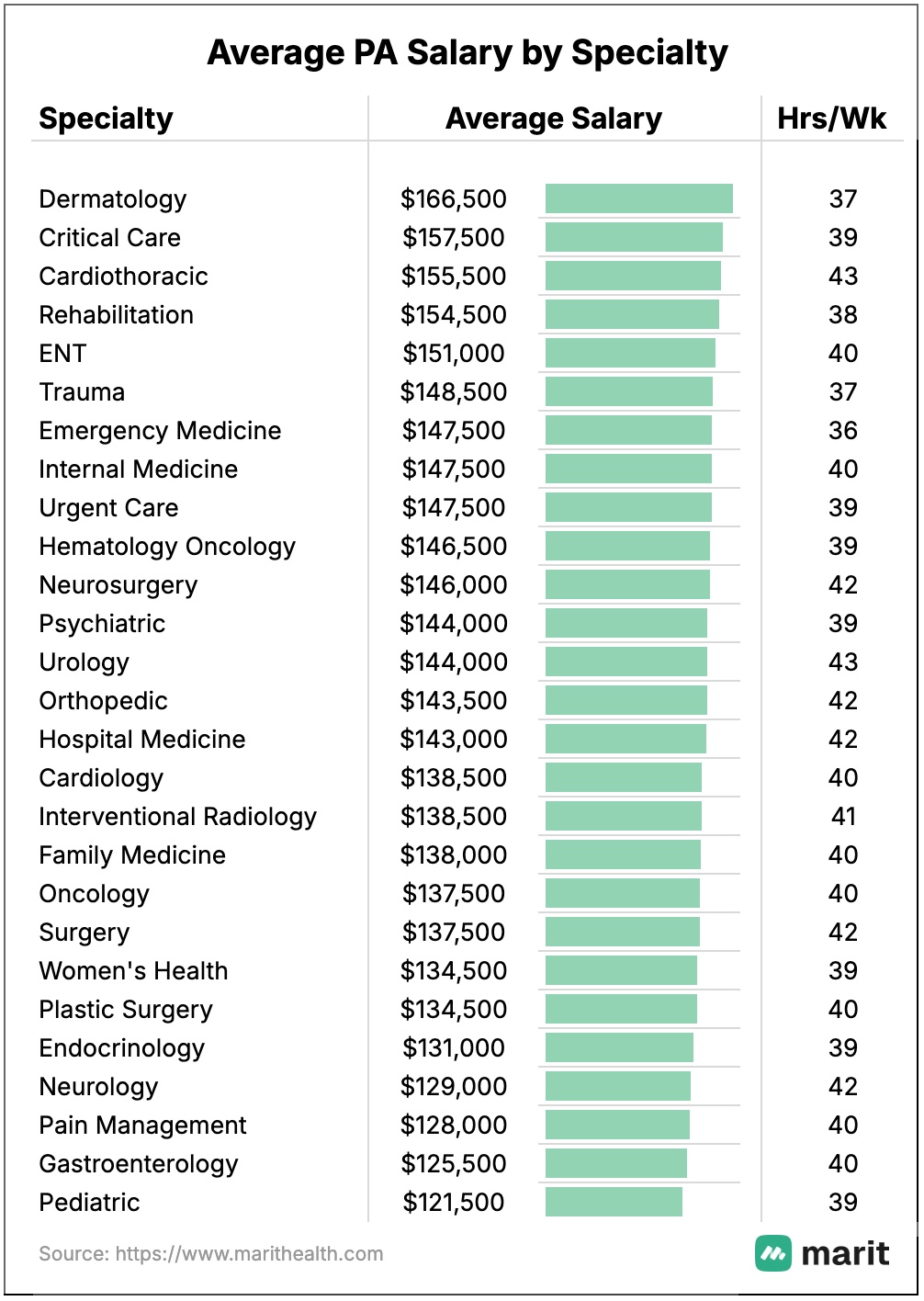

The 3 Highest Paying PA Specialties in 2025

Using Marit Health salary data, these are the current top-paying specialties:

- Dermatology — Average: $166K/year

- Avg. weekly hours: 37

- Also has highest percent of PAs earning $200K+

- Critical Care — (as a critical care PA myse...

Author

Kristin Burton

Founder

Kristin Burton is a pulmonary/critical care PA and founder of Millionaires in Medicine. She paid off $161,000 in student loan debt in 16 months, and then went on to become a millionaire at 31.

Have insurance needs?

Look no further than Protuity for your life and disability insurance.

Navigating physician contracts can be overwhelming. Resolve offers a personalized legal experience to equip you with the tools and support needed to secure the best terms for your career.

Use code MIM15 to receive a 15% discount at checkout.

Doc2Doc helps healthcare providers explore personal loan options to consolidate debt, simplify payments, and potentially lower what they’re paying in interest.

Prepping for EORs, PANCE, PANRE, or EOC?

Get the support you need right now to stop second guessing your test answers, ditch your anxiety, and learn the 7 critical test-taking skills you need to knock your PA exams out of the park.